Don’t Miss Tomorrow’s Supply Chain Industry News – Essential Updates and Trends">

Don’t Miss Tomorrow’s Supply Chain Industry News – Essential Updates and Trends">

Actionable directive: Track tariffs exposure now; adjust sourcing terms to limit risk in the whole logistics system.

Data cues: A 13-month decline in tires prices signals tighter margins; across manufacturing, transport, facility operations; Bangalore shipments show volatility; Arizpe (arizpe) plants remain affected by policy shifts; the oracle of market signals suggests shifts in procurement windows, advice to rotate suppliers; increase standardization in key components like tires, processors.

Operational priorities: Shorten replenishment cycles; close gaps in transport planning; align with manufacturing needs; push advice on supplier contracts prior to policy shifts tightening coverage. Monitor the 13-month trend in tires, processors; evaluate facility exposure at Bangalore; Arizpe remains a focal point.

Strategic actions: Build a system that tracks tariffs across regions; implement standardization for critical parts–tires, processors–so a single supplier disruption doesn’t cascade. The president’s trade stance could shift; contingency planning must consider alternate routes; also diversify sources beyond Bangalore, Arizpe, along with other hubs.

Final note: Follow advice from a practical oracle to prioritize near-term actions; diversify suppliers in Bangalore, Arizpe; consider another locale for critical manufacturing needs; close the loop with feedback from facility managers to reduce downtime.

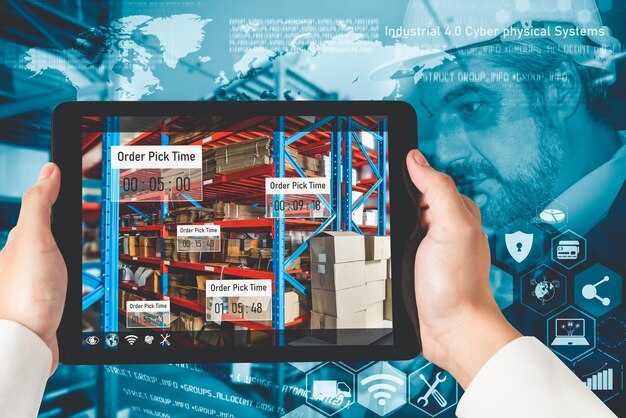

Tomorrow’s Supply Chain News: Updates and Trends

Prioritize a regional warehouse plan in oregon this december to capture rising demand; deploy autonomous carriers; enable a fusion of data streams to speed up forecasting; reduce closing cycles.

Resilience rests on visibility across warehouses; region signals show food sectors facing tighter margins because of capacity constraints.

Late Q4 shifts require practical recommendations: reallocate capacity; upgrade routing; price arbitrage for distributors; also review deal structures for regional networks.

arizpe ties to supplier networks; they cited closures impacting carrier reliability; a year-on-year shift favors shorter, more flexible deal terms.

Your plan should allocate budget to food warehouses; enable autonomous loading; monitor december orders; position your logistics for a fusion-informed regional supply response.

Don’t Miss Tomorrow’s Supply Chain Industry News: Updates and Trends; DHL Supply Chain deploys Volvo autonomous trucks in Texas

Implement a staged rollout of Volvo autonomous trucks in Texas with clear KPIs for throughput, operational safety, and costs per mile.

The deal here is tied to a broader regional plan: using autonomous trucks to move goods between farm and manufacturing sites and warehouses, reducing handling steps and processing times. In Texas, DHL’s move deploys Volvo autonomous trucks to link hubs with warehouses, aiming for most of the reductions in cycle times and cuts in tire wear, while theyre able to run with fewer operators on certain shifts, improving efficiency across the regional chains.

Operational impact spans staff changes: jobs shift toward monitoring, maintenance, and security, with a dedicated team overseeing autonomous freight. Management will coordinate cross-border routes within the network, including Canada and Puebla, and operators will staff control centers as shifts run around the clock. Starting in january and continuing into march, the model aims to maintain well-trained staff while reducing downtime in danville and alabama, positioning the operation for longer, steadier gains.

For other players, the approach favors a phased expansion across regional chains, linking danville, michigan and alabama sites with hubs in canada and puebla. The emphasis on autonomous operations supports well-controlled processing, reductions in downtime, and more predictable costs for foods and other manufacturing lines. Starting later in january, operators will test cross-border lanes and security controls, over the next quarter they aim to keep service levels high across all shifts while expanding to more hubs, within the world of modern logistics.

Route optimization gains: which Texas corridors and delivery windows benefit first

Recommendation: target Dallas–Fort Worth to Houston corridor first; I-35 Austin–San Antonio route follows quickly; implement dynamic delivery windows; concentrate going shipments in the 9:00–15:00 local slot; What matters here is prioritization of Texas corridors; most cases show material gains across the region; operational costs trend down 6–9% within 90 days; faster dock times, tighter schedules.

Approach specifics: routing models tied to live traffic feeds; closure alerts remove blind legs; eliminated miles prevent backtracking; tire wear signals tighten maintenance windows; within danville and hayward hubs, pilots cut miles by 8–12%; tennessee markets, apac business teams, volkswagen pilots reflect similar savings; diginomica notes support from markets; cfos observations: costs fall; president oversight accelerates scale; reading from diginomica confirms the pattern.

Implementation steps: three pilots across the Dallas–Fort Worth–Houston spine; fixed window schedules; weekly calibration; KPIs: miles per gallon, idle time, on-time deliveries; calls from customers drop as reliability rises; operating costs trend downward; tasks done; recognize what works; close the loop with cfos, president to scale; needed to sustain momentum; logistics chains in Texas.

Actionable takeaways: tighten dispatch permissions within peak windows; eliminate unnecessary stops; document closure constraints; maintain whole life-cycle data; recognize how this aligns with broader market objectives; for markets trying to lock schedules, the pattern matches what is described by diginomica; with volkswagen programs, apac leadership, the shift scales across Tennessee workflows; most producers see benefitting this quarter, costing reductions, plus improved service.

Safety and regulatory steps for pilots: permits, operator training, and oversight

Concrete recommendation: securing a formal aviation operator permit and enrolling in a published training program before any commercial flight is enabling robust safety and regulatory alignment. Start the process now; the certification cycle for new operations can take several weeks to months, depending on the region. In february, authorities explained changes to licensing and reporting and described how compliance comes with documented processes.

Permits and approvals cover airworthiness certification for the aircraft, an operator license, remote-pilot certificate, and BVLOS authorization when required. When BVLOS is needed, the process often adds a separate approval cycle and additional costs. Costs vary by jurisdiction; plan for application fees, document checks, medical screening where applicable, and proof of insurance. The published requirements typically include background screening and a defined operating envelope.

Training program design centers on a formal program with modules on air law, meteorology, navigation, aircraft systems, and emergency procedures; include human factors and crew resource management. Use simulators and on-the-job mentoring; set a recurrency cycle for refresher training every 12–24 months; maintain a training ledger. Identify the needed competencies and map them to the manufacturer guidance and the producer’s recommended operating practices to ensure operational competence.

Oversight strategy combines incident reporting, flight data capture, and routine audits; keep records for at least 2–3 years and coordinate with the regulator to schedule inspections. Streamlining of documentation and process handoffs reduces cycle time for compliance and supports steady operations in multi-site setups around regional corridors. If risk comes up, oversight steps in quickly.

Case snapshot: a regional rollout around a distributor network serving foods, autos, and truck components illustrates the path. The team went long on the recertification cadence; gillespie, walker, and lavergne drove the initiative, with processing checks and a focus on closure of legacy gaps. The effort enabled safer operations along a logistics network and created a sustainable legacy for the program, then repeated in neighboring regions.

Cost implications and ROI timeline for DHL’s Volvo deployment

Recommendation: launch a phased Volvo deployment anchored at Puebla center, starting with 20 units, then scale to 60 within 12 months across several markets; align with a published cost model; track accounting impacts within erps; move to a paperless data loop; thats decisive for governance. As example, Puebla serves as a live center to validate motor and assembly workflows, validate customizations, and measure human performance under real conditions in those markets. Establish clear requirements for the system, ensure close monitoring of utilization, and publish insights to ease standardizing across centers.

Cost structure centers on capital outlay, integration, and change management. Per-truck capital outlay ranges from $120k to $160k; for 60 units total near $8.4M; plus upfront systems integration $1.2M; training $0.3M; center of excellence $0.25M; cloud hosting $0.15M; paperless reporting setup $0.05M. Total initial around $10.35M. In this layout, Puebla assembly lines and center operations feed data into erps, enabling a single source of truth across those countries. Long lead items include standardized motors, telematics, and powertrain interfaces; those components drive early payback in fuel efficiency and maintenance cost declines.

ROI timeline hinges on utilization levels, route complexity, and the pace of standardizing processes. Insight from early runs suggests a baseline payback window of roughly 28–42 months for the full fleet rollout, with aggressive utilization scenarios delivering 28–36 months. Key drivers include fuel savings, reduced downtime, and shorter close cycles for accounting, enabled by standardized reporting and centralized paperless trails. Human factors matter: focused training reduces idle time, improves asset uptime, and accelerates the learning curve across multiple markets; this reduces the risk of decline in performance when scaling from one country to several others. Example: in the Puebla pilot, assembly line velocity improved by 12 percent after motor and control system standardization, creating a measurable uplift in daily miles per truck. The approach also supports rapid insight into requirements, allowing iterative improvements to ERPs, WMS, and TMS interfaces across center operations.

| Element | Cost (USD) | ROI Levers | Payback (months) |

|---|---|---|---|

| Vehicle cost; installation (60 units) | 8.4M | fuel efficiency, route optimization, reliability | 28–40 |

| Systems integration (ERPs; WMS; TMS) | 1.2M | data standardizing, cross-country visibility | 34–42 |

| Training; change management | 0.3M | operator readiness; faster utilization | 30–36 |

| Center of excellence; process standardizing | 0.25M | governance; reuse of configurations | 36–48 |

| Data center; cloud hosting | 0.15M | scalability; sharing best practices across markets | 24–30 |

| Paperless reporting; compliance trails | 0.05M | reduced manual work; faster close | 20–28 |

| Total initial | ~10.35M | - | - |

| Estimated annual savings (post-payback) | ~3.1M | fuel, maintenance, driver hours | - |

Key performance indicators to track during autonomous trucking trials

What to start with: a three-metric cockpit focusing on reliability; throughput; energy per mile. Extend with processing latency; disengagement rate; image quality; tires wear rate; regional benchmarks. For canada routes, a deal with distributors; volkswagen announced a regional pilot; this informs world-scale practice. Starting from a single corridor; management measures what took place on each operation leg. Maybe calls from customers shape future jobs in regional warehouses; they reflect expectations. Foods shipments through cold chains test resilience. The second wave of trials arrives with improved capabilities; starting points tighten the business case; these steps raise risk management; governance readiness. Also diginomica notes camera image reliability; this matters for transport networks across the world.

- Reliability; safety: MTBF; MTTR; disengagement rate per 1,000 miles; sensor fault rate; image quality score; tires wear rate; incident severity. Targets: MTBF 100–150 hours; disengagement rate < 0.1 per 1,000 miles; image quality score ≥ 0.9; tires wear rate ≤ 2% per 10,000 miles.

- Operational efficiency; throughput: on-time delivery rate; average dwell time per stop; miles per vehicle per day; vehicle utilization; route adherence. Targets: on-time ≥ 95%; dwell time per stop < 10–15 minutes; miles per vehicle per day > 350; route adherence ≥ 98%.

- Cost; maintenance; asset wear: tires wear rate; maintenance cost per mile; parts replacement rate; downtime due to faults. Targets: maintenance cost per mile ≤ 0.20–0.30; downtime < 2–4 hours per 1,000 miles; parts replacement rate ≤ 1.5% monthly.

- Planning; routing; decision-making: route accuracy vs plan; detour rate; first-attempt delivery success; planning latency. Targets: route accuracy > 99%; detours < 1%; first-attempt success > 95%; planning latency < 2 minutes.

- Data quality; processing: data latency; processing throughput; data quality score; image capture rate. Targets: data latency < 250 ms; processing throughput > 500 Mbps; data quality score > 0.95. Note: diginomica emphasizes camera image reliability as a driver for control decisions; image processing efficiency correlates with response time.

- Business impact; partnerships; regional expansion: cost-to-serve; revenue per mile; cross-border readiness with canada; deals with distributors; volkswagen announced a regional program; lessons for foods distribution via cold chains; management governance; scaling plan. Metrics: margin per mile; contract renewal rate; number of active regional pilots; improvements in intermodal handoffs with forklift at docks.